質問 1:Which costing method, used in just-in-time (JIT) production systems, attaches cost directly to output rather than following the flow of product through the production process?

A. Absorption costing

B. Backflush costing

C. Marginal costing

D. Process costing

正解:B

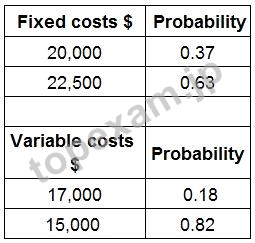

質問 2:GP is launching a new product. The annual forecast costs are as follows:

What is the expected value of the total costs?

Give your answer to the nearest whole $.

正解:

$36935

質問 3:Which of the following statements about expected value is NOT correct?

A. It assumes that the decision is repeated a very large number of times.

B. It represents the distribution of possible outcomes by a single figure.

C. It is the weighted average outcome based on the probability of each outcome.

D. It draws management attention to the possibility of very high or very low outcomes.

正解:D

質問 4:A manager has to decide between four mutually exclusive projects, A, B, C and D:

Using the above information, which Project would a risk seeking manager choose?

A. Project A

B. Project D

C. Project C

D. Project B

正解:B

質問 5:Which THREE of the following statements relating to fixed overhead variances are correct?

A. The total fixed overhead variance is made up of the fixed overhead expenditure variance, the fixed overhead efficiency variance and the fixed overhead capacity variance.

B. The fixed overhead volume variance can be split into the fixed overhead efficiency variance and the fixed overhead capacity variance.

C. The total fixed overhead cost variance in an absorption costing system is the difference between budgeted fixed overhead and actual fixed overhead incurred.

D. The total fixed overhead cost variance in an absorption costing system is the amount of fixed overhead that has been under- or over-absorbed in the period.

E. In a marginal costing operating statement reconciling budgeted contribution to actual profit only the fixed overhead expenditure variance and the fixed overhead volume variance are shown.

正解:A,B,D

質問 6:TDM edits, prints and publishes three magazines, Mag A, Mag B and Mag C. The company operates an activity-based costing system.

The following information has been obtained.

What is the overhead cost attributable for each Mag A publication?

Give your answer to the nearest whole cent.

正解:

83 cents

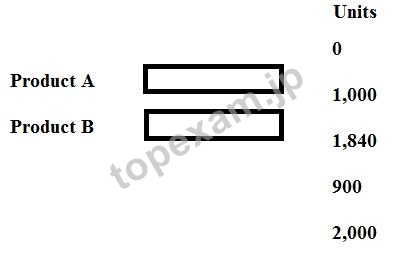

質問 7:Demand for two products, A and B is 1,000 units and 2,000 units respectively. Each unit of Product A requires 8 kg of material and each unit of Product B requires 5 kg of material. The maximum availability of material is 17,200 kg. Contribution per unit of A is $10 and per unit of B is $9.

Place the production volumes of Product A and Product B, that will maximize contribution, in the table.

正解:

正解:

質問 8:

質問 8:A medium-sized manufacturing company, which operates in the electronics industry, has employed a firm of consultants to carry out a review of the company's planning and control systems. The company presently uses a traditional incremental budgeting system and the inventory management system is based on economic order quantities (EOQ) and reorder levels. The company's normal production patterns have changed significantly over the previous few years as a result of increasing demand for customized products. This has resulted in shorter production runs and difficulties with production and resource planning.

The consultants have recommended the implementation of activity based budgeting and a manufacturing resource planning system to improve planning and resource management.

How will a manufacturing resource planning system improve the planning of purchases and production for the company?

Select ALL the correct answers.

A. The technique will not enable managers to track orders through the manufacturing process and will not assist the purchasing and production control departments to move the right amount of material or sub-assemblies at the right time to the right place.

B. It seeks to ensure that resources are available just before they are needed by the next stage of production or dispatch. It also seeks to ensure that resources are delivered only when required so that raw material inventory is kept to a minimum.

C. The traditional approach to determine material requirements is to monitor inventories constantly; whenever they fall to a predetermined level, a preset order is placed to replenish them. This traditional approach (involving re-order levels and economic order quantity calculations originates in the pre- computer era.

D. A manufacturing resource planning approach to the management of all the company's manufacturing resources including inventory, labour and machine capacity.

E. The correct inventory management system relies on the assumption that there is constant demand.

An MRP system begins with the setting of a master production schedule specifying both the timing and quantity demanded of each of the finished goods items and then works backwards to determine the resource requirements at each stage of the production process.

F. It aims to generate an estimation of materials requirements after taking account of the number of employees quality and waste. The TQS model can be used within MRP provided that the major assumption in the TQS model of constant demand applies.

正解:B,C,D,E

質問 9:A manager must select one of three projects, W, X or Y.

The following payoff table has been prepared to show the outcomes in $000 at three possible levels of demand:

The manager is now preparing a regret matrix.

What figure (in $000) will be shown for Project Y in the regret matrix if the average demand arises?

A. 160

B. 150

C. 110

D. 520

正解:B

安全的な支払方式を利用しています

Credit Cardは今まで全世界の一番安全の支払方式です。少数の手続きの費用かかる必要がありますとはいえ、保障があります。お客様の利益を保障するために、弊社のCIMAPRO19-P01-1問題集は全部Credit Cardで支払われることができます。

領収書について:社名入りの領収書が必要な場合、メールで社名に記入していただき送信してください。弊社はPDF版の領収書を提供いたします。

弊社は無料CIMA CIMAPRO19-P01-1サンプルを提供します

お客様は問題集を購入する時、問題集の質量を心配するかもしれませんが、我々はこのことを解決するために、お客様に無料CIMAPRO19-P01-1サンプルを提供いたします。そうすると、お客様は購入する前にサンプルをダウンロードしてやってみることができます。君はこのCIMAPRO19-P01-1問題集は自分に適するかどうか判断して購入を決めることができます。

CIMAPRO19-P01-1試験ツール:あなたの訓練に便利をもたらすために、あなたは自分のペースによって複数のパソコンで設置できます。

弊社は失敗したら全額で返金することを承諾します

我々は弊社のCIMAPRO19-P01-1問題集に自信を持っていますから、試験に失敗したら返金する承諾をします。我々のCIMA CIMAPRO19-P01-1を利用して君は試験に合格できると信じています。もし試験に失敗したら、我々は君の支払ったお金を君に全額で返して、君の試験の失敗する経済損失を減少します。

CIMA CIMAPRO19-P01-1 認定試験の出題範囲:

| トピック | 出題範囲 |

|---|

| トピック 1 | - Determine the activity that causes the change in cost

- Understand the difference between variable costs and fixed costs

|

| トピック 2 | - Understand the impact of individuals’ risk attitudes on decision-making in the short term

- Understand the difference between direct costs and indirect costs

|

| トピック 3 | - Calculate subdivision of total usage

- efficiency variances into mix and yield variances

- Use material, labour, variable overhead, fixed overhead and sales variances

|

| トピック 4 | - Calculate the breakeven point and output level required to meet income targets

- Understand costing and the different reasons for calculating costs

|

| トピック 5 | - Establish manufacturing standards for material, labour, variable overhead and fixed overhead

- Understand the difference between financial accounting and cost accounting

|

| トピック 6 | - Understand relevant cash flows and non-financial factors and how it affects make or buy decisions

- Understand the strategic implications of short-term decision-making

|

| トピック 7 | - Calculate revenue and cost estimates using quantitative analyses

- Calculate and interpret overall flexed budget variances

|

参照:https://www.cimaglobal.com/Qualifications/Professional-Qualification/Operational-level/

TopExamは君にCIMAPRO19-P01-1の問題集を提供して、あなたの試験への復習にヘルプを提供して、君に難しい専門知識を楽に勉強させます。TopExamは君の試験への合格を期待しています。

一年間の無料更新サービスを提供します

君が弊社のCIMA CIMAPRO19-P01-1をご購入になってから、我々の承諾する一年間の更新サービスが無料で得られています。弊社の専門家たちは毎日更新状態を検査していますから、この一年間、更新されたら、弊社は更新されたCIMA CIMAPRO19-P01-1をお客様のメールアドレスにお送りいたします。だから、お客様はいつもタイムリーに更新の通知を受けることができます。我々は購入した一年間でお客様がずっと最新版のCIMA CIMAPRO19-P01-1を持っていることを保証します。

弊社のCIMA CIMAPRO19-P01-1を利用すれば試験に合格できます

弊社のCIMA CIMAPRO19-P01-1は専門家たちが長年の経験を通して最新のシラバスに従って研究し出した勉強資料です。弊社はCIMAPRO19-P01-1問題集の質問と答えが間違いないのを保証いたします。

この問題集は過去のデータから分析して作成されて、カバー率が高くて、受験者としてのあなたを助けて時間とお金を節約して試験に合格する通過率を高めます。我々の問題集は的中率が高くて、100%の合格率を保証します。我々の高質量のCIMA CIMAPRO19-P01-1を利用すれば、君は一回で試験に合格できます。

PDF版 Demo

PDF版 Demo

品質保証TopExamは我々の専門家たちの努力によって、過去の試験のデータが分析されて、数年以来の研究を通して開発されて、多年の研究への整理で、的中率が高くて99%の通過率を保証することができます。

品質保証TopExamは我々の専門家たちの努力によって、過去の試験のデータが分析されて、数年以来の研究を通して開発されて、多年の研究への整理で、的中率が高くて99%の通過率を保証することができます。 一年間の無料アップデートTopExamは弊社の商品をご購入になったお客様に一年間の無料更新サービスを提供することができ、行き届いたアフターサービスを提供します。弊社は毎日更新の情況を検査していて、もし商品が更新されたら、お客様に最新版をお送りいたします。お客様はその一年でずっと最新版を持っているのを保証します。

一年間の無料アップデートTopExamは弊社の商品をご購入になったお客様に一年間の無料更新サービスを提供することができ、行き届いたアフターサービスを提供します。弊社は毎日更新の情況を検査していて、もし商品が更新されたら、お客様に最新版をお送りいたします。お客様はその一年でずっと最新版を持っているのを保証します。 全額返金弊社の商品に自信を持っているから、失敗したら全額で返金することを保証します。弊社の商品でお客様は試験に合格できると信じていますとはいえ、不幸で試験に失敗する場合には、弊社はお客様の支払ったお金を全額で返金するのを承諾します。(

全額返金弊社の商品に自信を持っているから、失敗したら全額で返金することを保証します。弊社の商品でお客様は試験に合格できると信じていますとはいえ、不幸で試験に失敗する場合には、弊社はお客様の支払ったお金を全額で返金するのを承諾します。( ご購入の前の試用TopExamは無料なサンプルを提供します。弊社の商品に疑問を持っているなら、無料サンプルを体験することができます。このサンプルの利用を通して、お客様は弊社の商品に自信を持って、安心で試験を準備することができます。

ご購入の前の試用TopExamは無料なサンプルを提供します。弊社の商品に疑問を持っているなら、無料サンプルを体験することができます。このサンプルの利用を通して、お客様は弊社の商品に自信を持って、安心で試験を準備することができます。